By John Spangler

Associate Editor, Volume 23

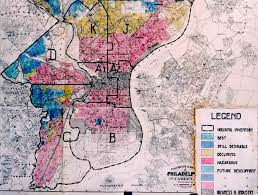

Production Editor, Volume 24 Patrick Miles Jr. - Michigan candidate for Attorney General Detroit remains the most segregated metropolitan areas in the United States.[1] This is in part thanks to historical practices such as “redlining” where majority African-American neighborhoods were deemed “too risky” for mortgage lending.[2] Though overt discrimination in housing has been outlawed[3], the systems created for that purpose often remain, in whole or in part. One Democratic candidate for Michigan Attorney General, Pat Miles, has pledged to use the office to combat modern-day redlining.[4] Patrick Miles Jr., who prefers to go by Pat, is the former U.S. Attorney for the Western District of Michigan, serving from 2012 to 2017. Prior to that appointment, his experience was largely in private sector and telecommunications law. As part of our ongoing series examining the campaign pledges of candidates for that office, we have to ask: can he do that? The study Mr. Miles cited in his pledge to defend consumers was conducted by Reveal, a project of the Center for Investigative Journalism. Its analysis of data from 61 metro areas across 2015 and 2016 resulted in a blunt conclusion: “Fifty years after the federal Fair Housing Act banned racial discrimination in lending, African Americans and Latinos continue to be routinely denied conventional mortgage loans at a rate far higher than their white counterparts.”[5] In Detroit, that trend meant an African-American applicant was almost twice as likely to be denied a conventional home mortgage.[6] Defenders of current mortgage practices point to what they believe are flaws in that data. They argue that high rejection rates are a result of large lenders and technology, making applying for a mortgage easier and leading to more applicants with subpar credit.[7] Yet this explanation ignores that federal housing policy codified racial minority populations as a lending risk for years, and those policies’ effects persist today.[8] Without the access to long-term investment and wealth from generations ago, today’s minority borrowers are still subject to these trends.[9]